It seems like this has been a week of introduction posts. Today’s “introduction” of sorts is to a Calendar. You might have many different calendars, all synced and reminding you of what you need to do. But today we learn about the Milenomics Credit Card Calendar.

The Credit Card Calendar (CCC) is very simple. The year is split into 3 month sections. The calendar works best with 2 persons sharing it, so if you’re married or have a fiance who’s willing to learn and use Milenomics you’ll have an easier time.

Step 1: find your average spending per month.

How much is your average “real” spending per month. This is without any CVS purchases, or Wal-Mart trips. Just plain ordinary boring bills, rent, gas, etc. This is the baseline spending we’ll use to craft our Credit Card Calculator.

You can easily start out with an average spend of as little as $1,000 per month. I’ll be using a slightly higher amount for today’s examples, but I don’t want you to be discouraged thinking you don’t “spend enough.” In fact knowing your baseline spending is very important. Without it you have no way of telling if you’ve started wasting money by eating out 10 times more per month than usual, or buying expensive electronics for the miles. It is of paramount importance that you do not alter your day to day spending because of miles. Doing so is a hidden cost of miles, and can very quickly eat up profits and cause high CPM.

Step 2: Craft your Calendar

We’ll use today as the starting point of the CCC. Your months will be:

- September

- December

- March

- June

Easy to remember because they follow the seasons of the calendar. As we move into a new season we move into (and out of) new credit cards. Always keep the flyertalk thread on best credit card offers handy, and review it in the months to follow. Today we’ll put together a CCC for a spender of $2,000 per month.

September: Total spend in 3 months: $6,000

- -First Card to get: Citi AA Mastercard, 50,000 miles after $3,000 spent (90 days)

- -Balance left $3,000

- -Second card to get: Chase United MP Explorer 50,000 miles after $1,000 spent (90 days)

- -Bonus: Extra 5,000 for adding an authorized user, 2 UA Lounge passes.

- -Balance left, $2,000

Note: getting this application to come up is tricky, you’ll want to read the post carefully. I verified as of this AM it does still come up.

- -Third Card to get: Chase British Airways Visa 50,000 miles after $2,000 spent (90 days).

- -Balance left, $0

I use this card for my writeup “Why are frequent flyer miles so hard to use?” Read more about the utility of these miles there.

- -Fourth card to get: Barclay’s US Airways Mastercard, 35,000 miles after $1 spent. Bonus 10,000 miles at 1 year anniversary (use the third link).

This card really is like the cherry on top of an ice cream sundae. I always add it to any round of Credit card apps. Why? With no real minimum spending requirement there’s not much harm in applying for it. I leave it for last, so that all the other apps go through first.

Note: I gain nothing from your applying for these cards

Total haul for September:

- 53,000 AA miles

- 56,000 UA miles

- 52,500 BA Miles

- 35,001 US miles

196,501 miles. $6000 in spending, for a total of 32 miles per dollar. If you remember, yesterday I talked about supply and demand of miles. If this is too much supply for you, I’d recommend switching out some of these cards for cash back cards instead to earn cash instead of miles. If it is not enough supply you may want to rethink the cards I mention here, and go for more/others. As always, don’t take on more than you can handle. If you miss the minimum spending requirements you’ll earn 0 miles.

In three months I’ll be writing our winter season applications. If you have a spouse/SO December will be the month they apply. You’ll alternate; Fall and Spring for you, Winter and Summer for your SO. This spreads out the applications by 6 months for each of you. Assuming a similar pull of miles in the Winter season you’ll continue to earn 30+ Miles per dollar all year long.

What about the Chase Sapphire Preferred? Isn’t it the greatest card ever?

Put simply: No, it isn’t the greatest card ever. With Milnomics there is no “greatest card ever.” There is a time for everything and a season for everything. September is not the season for CSP. Why? There is a 7% bonus on all miles earned with the CSP. Opening the card right now means your bonus will only be from September-February. I’ll include the CSP in our spring applications, so we maximize the 7% bonus.

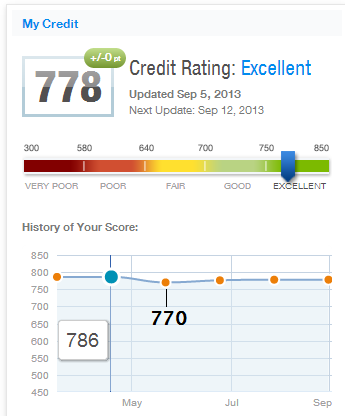

What about my credit score?

I’m glad you asked. You’ll want to sign up for free credit scoring (yes, it is a FAKO, but pretty good for free), at https://www.creditkarma.com/. I’ve used the site for years, and get nothing from your signup. You’ll be able to keep an eye on your credit score there. Applying for credit cards will ding your score a bit. My last round of applications hit me for 16 points. Three months later and most of that 16 points has been recovered.

The extra available credit from new cards along with paying on time help. As always educate yourself about your credit, and don’t do anything if you’re looking to refinance/buy a home soon. 4 credit card apps might not hurt your credit much, but it isn’t worth the risk in that type of situation.

A final word about annual fees: don’t worry about the annual fees for these cards, I’ll be writing more about them tomorrow, and how Milenomics avoids them as best as possible. In 4 years I’ve paid $0 in Annual fees…correction, I’ve actually made money on annual fees (check back tomorrow).

If you have any questions follow me on twitter, @Milenomics.

Everything below this line is Automatically inserted into this post and is not necessarily endorsed by Milenomics:

Made money on annual fees?! I’ll be tuning in tomorrow!

Seems a bit misleading that you start with “spend as much as makes sense to you” and then immediately follow it up with “I’m using a higher number to demonstrate the cards” as only with the higher number do you get all the bonus points.

@WA: Thanks for the feedback. The example I used was for a $2,000 a month spender. Someone who spends less should remove one card and just apply for the other three. If they’re more experienced they could do a small amount of MMRs to hit the bonus on all four, but this being an introduction post I didn’t want to go there. I do agree with you, the pull of the higher number can cause people to spend outside their means, which is why I included the bold phrase: “It is of paramount importance that you do not alter your day to day spending because of miles.”

I see this everywhere…. but why does WA constantly badger all other bloggers???? jeez. Focus on improving your own cr*p blog instead of bashing literally everyone elses.

See what I meant about not seeing any dates/time stamp on your articles??? Chase no longer gives the 7% anymore to new applicants? Except you’re grandfathered in, then you get it for a couple more years, then zit!

So then that shouldn’t be a factor for screening out CSP in Sept…

Alex: Should be all fixed now. Again I appreciate you bring this up–I totally missed the fact that dates disappeared. This is a pretty old post–but an important one indeed.

I noticed! 🙂 thanks for fixing it.. It helps out a lot knowing the timeframe! :))

Your pages are sooo informative, I’m reading them ALL lol, old and new 🙂

Three months later your score recovered.. Do you ever bump them off yourself? Or Chase doesn’t mind if you applied for two of their cards 3-4 months ago, and you’re already applying for 2-3 more? I’m trying to figure out how to go about it and not raise flags..?

Alex, no I don’t bump any off myself. I find that the added lines and on time payments more than make up for the pulls.