Those of you who have been with Milenomics from the start will remember that Milenoics strives to avoid annual fees whenever possible. Today I’m updating you with my personal experience getting annual Fee Waivers on my Citibank Visa Cards. I’ll continue to update all of my Annual fee waivers this year for you to see how the process works, and how it can absolutely save you money, earn you miles and let you keep your cards, or at least your credit line open.

The techniques used to do this are:

- 1) Calling and asking for an annual fee waiver.

- 2) Downgrading the card to something without an annual fee

- 3) Merging the credit line with another card we have.

I’m sure some of you will argue that the benefits of a card are worth the Annual Fee. However, the calls I outline below took me 6 minutes each and netted me $95 in annual fee waivers. With my T-Rate of $25/hr I spent $2.50 of my time to earn back the each annual fee.

Citibank Annual Fee Waivers

My yearly call to Citibank for a of my AA cards came due, and I thought I’d update readers with what my ultimate results were.

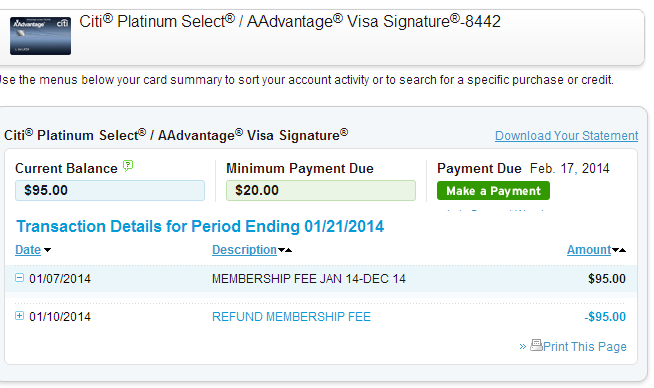

Card #1 Citi AAdvantage Platinum Visa: This card saw almost no use last year, under $500 in charges total. I called and the exchange went pretty much this way:

Me: “Hi, I noticed that the $95 annual fee was charged on my recent statement, and I really don’t use the card very much. I’d like to know if you could waive the fee somehow.”

Agent:“I’m sorry, but the fee is a valid charge, and covers many great benefits of having this card. Since the charge is valid I’m unable to remove it.”

Me: “Ok, I understand. If you can’t waive the fee I’d like to cancel the card then.”

Agent:“Am I to understand you wish to cancel the card because of the $95 annual fee?”

Me: “Yes, that’s right.”

Agent: “Please allow me to first transfer you to a specialist who may be able to offer you a fee waiver. If you do not wish to take any of those offers you may then cancel the card.”

(Transfer to Retentions officer)

Retentions:“I’d hate to see you go, and would like to offer you a waiver of the $95 on the spot, and an offer of 1,000 extra AA miles for each month you spend $1,000 or more on the card for the next 16 billing cycles.”

Me:“Oh wow, that’s so generous of you, I was going to cancel, but you’ve totally changed my mind. My faith in your company is restored!” (Ok, I’m punching that last one up for effect here on the blog).

The agent also did a review of my credit line and bumped it up $3,500 without a hard pull. I’ll take any extra credit I can get from Citi, as I’ll be applying for another Citi Card sometime this year, and could do a carve out of the unused credit line or close an account to open the new card.

Card #2 Citi AAdvantage Platinum Visa: I didn’t use this card at all last year. The annual fee hit, and I called in and spoke to a somewhat surly phone agent. She insisted that the annual fee could not be waived. I requested to cancel the card, and was then offered a fee waiver if I spent $3,000 on the card in the next 3 months. I pushed for a different offer, and asked about the 1,000/$1k offer. I was told I did not “qualify” for the offer.

Having doubles of this card I could have asked to merge the credit line, instead I asked to downgrade to a Bronze card, remove the annual fee and keep the card open. The agent downgraded me to the AA Bronze card. I won’t use the card ever, and keeping the credit line open will help me for my next round of applications, should I need to close a card to get an approval from Citi.

Was it possible to get a better offer than this? I think it might have been, but since I almost never use the card I felt the downgrade was a smart second option.

Citibank–11 Month Itch Friendly

The yearly dance with Citi continues. Citi and I go around and around and around. They claim there are wonderful benefits to their cards; I call and ask for a waiver of the fee or I’ll cancel. They then waive the fee.

Take note: There needs to be some truth to the cancellation threat. Some banks will walk you right to the edge, and really push you to cancel before you get a waiver. My experience is that Citi usually puts an offer up without too much struggle, but I’m always ready to cancel, downgrade or merge. My threats are not empty–and yours shouldn’t be either.

The two offers being pushed right now by Citi seem to be the two I received, either spend $X,000 in 90 days and receive a waiver, or receive the waiver on the spot and the 1,000 bonus miles for $1,000 in spending each month.

A third option is the downgrade to an AA Bronze card, a novelty card really, earning half a mile per dollar and with no other real benefits. Still, keeping the credit line alive can be important for our credit score, and for future CCC applications.

General Tips to Receive Annual Fee Waivers

What follows are my tips for receiving waivers of Annual Fees. Feel free to share your own tips in the comment section:

1. Be polite. No one enjoys talking to a grump on the phone, and you catch a lot more flies with honey than vinegar.

2. Be Direct. Don’t beat around the bush about how you wish the annual fee was lower, or you’re “thinking” of cancelling the card because of the Annual fee.

3. Be ready to cancel (or at least downgrade). There needs to be some truth to your threat.

4. Say what you want. If you want an offer that you know someone else got–bring it up. If you want bonus miles instead of an annual fee waiver say that instead. You can negotiate to some extent with Retentions agents, but they’re not mind readers.

5. Know a good offer when you receive one, and accept it.

Update: Twitter user Gil C offered another great tip:

@Milenomics helpful to know that the offers are preloaded, just keep asking “what else can you offer me” to make sure you take the best one

— Gil C (@gil949) January 24, 2014

For a really interesting read here’s a blog post from an ex Citi retentions agent. Retentions departments exist because it is almost always cheaper to keep a customer than to acquire a new one. Keeping you as a customer has value–and we’re trying to exploit that value to our advantage.

Keeping Benefits Without Paying Annual Fees

We’ve discussed card benefits before, and we should be using them to simulate Elite benefits, using the Milenomics BYOE approach to travel. A big part of BYOE is keeping the benefits of these cards without paying an annual fee. The best way to do that is to receive annual fee waiveres.

The next best way is to be strategic about when you apply for cards, especially when playing the CCC in 2 player mode. For cards that are difficult to receive a fee waiver you should alternate years you hold the card. Applying in alternate years between yourself and your spouse/partner and ensuring you hold just one at a time would be a good strategy to gain the benefits but avoid the fee.

Know when to hold them and know when to fold them: I’ve got a backup City AA Visa, as well as my Citi AA Amex and my wife’s matching card as well. Should I not get an annual fee waiver and be forced to close a single card (such as the Visa I downgraded today) I’ve still got 3 backups giving me the benefits of free checked bags, boarding, and 10% back in AA miles per year. Knowing when you absolutely need a waiver and when you can downgrade is important before your call to ask for a fee waiver. Today I knew I only really needed a waiver on one card, so I was able to downgrade the other.

This type of strategy might not even be necessary with Citi AA cards. Getting a fee waiver seems to be consistently easy with these cards. For 4 years I’ve never paid an annual fee. Twice now I received a bonus where I would earn 1,000 extra miles per month for 16 billing cycles. After completing this bonus I’ll have earned 32,000 bonus AA miles over the life of the cards just because I called and asked for my Annual fee to be waived.

What’s better? Paying $95 a year, for 3 years or paying $0 and earning 32,000 extra miles?

Wrap Up

At the end of the day Annual Fees add up. Milenomics might love credit cards, but it hates Annual Fees. When the 11 month itch comes around be smart, and save yourself hundreds of dollars a year.

Annual Fees take our money and give it to others. Let’s Keep our Money and earn as many miles as possible. That’s Milenomics.

Everything below this line is Automatically inserted into this post and not necessarily endorsed by Milenomics: