All this week we’ve been talking about Resource Management of Miles. Resource Management is the grouping of resources to spread out risk and/or maximize return on investment. We began with the Icarus Paradox, and then moved onto ways to avoid account closures as well as the importance of setting up a system of accounts for your mile earning programs. Earlier today I talked about the benefits and drawbacks of earning and using miles for a couple.

A specific technique that I often am asked about is pooling miles from two credit cards, one in each person’s name into a common account. Can this be done? In some cases yes. In others no. Today we’ll also look at the risks to doing this.

The Benefits and Risks of pooling miles

Let’s first talk about why you might want to pool miles. Pooling miles means you reach the thresholds for awards quicker. If you and a spouse are both churning, but churning into separate accounts then you run the risk of an imbalance in miles from one account to the other. You’ll also run the risk of having one or more an accounts with orphaned miles–balances too low to use, but stuck in the program forever. Orphaned miles are a sad thing to have–Remember, Miles are not free, you spend time and money on earning them.

Milenomics is about saving Money and Miles. Over the years in researching ways to eliminate orphaned miles I came up with most of the information in this post. If there is a program you have experience in please share it with the rest of us Milenomics.

Chase UR:

Probably the best written about program for pooling points is Chase UR. I’ve covered pooling those points to allow you and a spouse to keep earning UR while only one of you holds a premium card at a time. The ability to pool is an intended part of the program. Whether it is wise to hold a massive amount of UR points instead of transferring them is a different discussion–and one which occurred during the comments section of the Financial Firewall post earlier this week.

- Pros: Pooling among spouses and households is allowed. Can also transfer from non-premium to premium UR cards and then transfer those into UA/Hyatt. Pooling is highly recommended for a family.

- Cons: Can lead to AA when names don’t match, or Chase gets the idea that transfers are being abused. Likelihood of that happening during legitimate transfers between partners/spouses is very, very low. Must have a premium UR card to get points out of the pool and into a travel program.

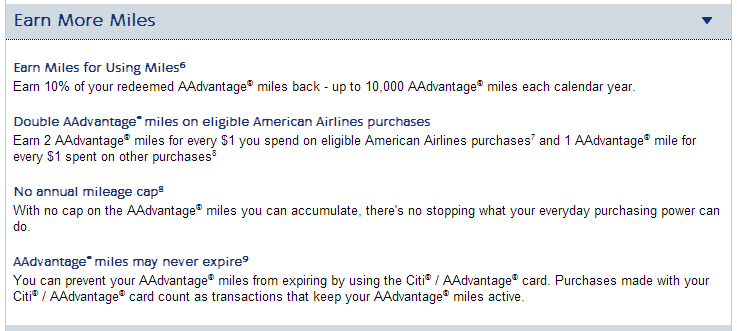

Citi AAdvantage Cards

You used to be able to complete an application for these cards and put pretty much anyone’s AA number on the form. The last time I attempted this, earlier this year, I was given a new AA number and unable to get Citi to change to the pooled account I set up long ago. There’s also been discussion of accounts being closed due to pooling miles, so even if you can still get this to work there’s that to worry about.

- Pros: Pooling miles from multiple cards (especially sign up bonuses) used to be able to help you earn EQM when Credit Card Miles counted towards AA lifetime status. I’m keeping this as a pro even though it doesn’t work any longer. Another pro is that you can pool miles so you’ll be closer to the amount you’ll need for an award quicker.

- Cons: AA on the part of Citi–closing of accounts, or worse forfeiture of miles. Also with the 10% award refund that AAdvantage cards have had for a few years you’re giving up an additional 10,000 AA miles per year if you pool into one account rather than keep things separate.

Southwest Rapid Rewards

This one should technically be do-able, but again isn’t supposed to work. You can credit your spouse’s application to your RR account, and then sign up yourself to get closer to a CP. Should you do this? Only you can answer that question. Getting a Biz/Personal in your own name makes more sense for a couple reasons. First, if the ability to combine apps from different people into one RR account stops then you’ll be stuck when it comes time to try to earn another CP via card apps. Secondly, the CP and the 110,000 SWA points you’ll need to earn it could be clawed back from you.

- Pros: Can earn CP faster and easier with 1 app from 2 people. Good if you don’t have a Business or can’t get approved for a Business SWA card.

- Cons: Risking not just your points, but also that extremely valuable CP.

British Airways Executive Club

BA is unique in that it specifically allows household/pooled accounts. This makes pooling miles easy, and worry-free. This also means BA Accounts with just a few Avios are easily drained as part of a redemption, and can be topped back up via any means (Chase BA visa, MR, actual flight miles).

- Pros: No worries about shutdown for pooling miles. Any redemption starts the 36 month clock over on both accounts since the number of miles is taken as a ratio of each account’s balance vs. the total. Also means that small point balances can be used up easily.

- Cons: A very serious con is that only members of the household account can fly on an award ticket. This means once you switch from a regular BA Executive Club account to a household account you can’t book tickets for anyone except the people in your household account. You also must wait 6 months to add or remove members from the household. Finally, you cannot have “your own avios.” Your Avios are used as a percentage of all redemption done from the Household account. So you might both have 100,000 BA Avios, but if your spouse redeems for a 30k Avios award you now both have 85,000 Avios. For a couple who like to keep their miles separate this could be the start of trouble.

Barclaycard US Airways Dividend Miles

This one is very easy to pool miles with. When you apply simply put the USDM number of your spouse on the application. I’ve done this numerous times without any issue, even with an address mismatch. This is not supposed to work and could end up with your miles being taken away. The coordination on Barclay’s side doesn’t seem to be there. I’ve had agents dig deep into my account and never “see” that my cards and my spouse’s are linked.

- Pros: Since US doesn’t seem to want to give up on round trip awards pooling miles helps you earn enough miles to get some use out of your USDM. An account with 80,000 miles in it is no good for trying to fly to Europe in J or Asia in F. Also the benefit of 5,000 mile reduced awards is based on the booking, not who flies, so the benefits of the card are not diluted by the pooling.

- Cons: AA, which seems very unlikely. You also may not receive 2x as many promotional offers–since those offers may be tied to 1 per USDM (not sure on this, but I notice that my card or my wife’s get the offers, not both). Really I get very little use from these cards, since the best USDM card is actually a Discover Card.

United MP Explorer

I’ve never heard of successful pooling of miles from United credit cards with different names. If you have please do let me know, either via comments, or via email. Leaving orphaned miles in a United Account isn’t that big of a deal anymore when you have a Chase UR card. You could transfer strategically into whichever UA account is low and bump up to a level you could then use to redeem.

American Express Membership Reward Points

Amex does not allow transfers between MR->MR. Similar to the UR Discussion above, you could easily transfer into each other’s programs to help rescue orphaned miles. Orphaned MR need to wait for you to open a new Premium MR product. You can save them however–by reading this post.

The Big Question: Does Pooling Miles Matter Anymore?

Pooling miles has some legitimate uses–earning miles faster for an award, or pooling miles so you don’t have an account left with orphaned miles. But the game has changed a lot in the past 5 years. In a lot of ways the reasons you used to want to pool miles are mostly all gone.

As discussed above now that Credit Card Spending doesn’t count towards lifetime status with any major airlines does pooling even make sense? Of the above cards discussed BA Household account and Chase UR pooling are definitely helpful to have as well. These programs help keep miles from becoming orphaned. The only unadvertised program I see a use for pooling would be the US Airways Dividend Miles pooling. If tomorrow USDM got rid of round trip awards I’d probably say there’s little to no reason left to pool with them either.

With AA, UA, and WN all allowing one way awards the importance of a pool account is lower now than ever before. There are very real negatives to pooling miles. In all cases accounts can be closed. But in the specific case of AAdvantage cards you’ve giving up 10,000 AA miles per year by not having separate accounts.[rule]