Update: A Happy ending, two new cards arrived 8/20. When I activated both I was charged $5.95, but a quick phone call got the two $5.95 activation charges reversed.

I hadn’t planned on back to back cautionary tales, but the luck of the draw has me writing this post today. A few weeks ago I wrote a post about how variable load Mastercards were being sold for a discount at some Safeway branded stores. In addition I mentioned that these cards were earning Fuel rewards. As a test for that post I bought two Mastercards at my local Vons, and detailed this purchase in the above post.

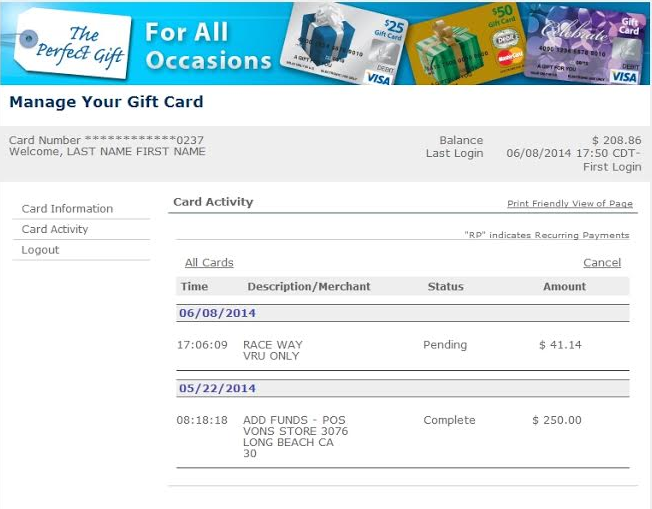

Yesterday I went to liquidate the exact two cards I bought as test cards. I called to set the PIN, and was told that my balance was $207 on each card. This struck me as very odd, so I logged in online and saw that the card had been used yesterday morning:

The second card also had a similarly vague $41 charge or so to a company that allegedly sells stickers. In reality these are likely shell companies which are just used to process CC’s. My card numbers had somehow been compromised and the cards would likely have been drained clean in the next few days.

High Level Fraud

These two cards sat in my safe deposit box for two weeks. I took them out this morning, planning to use them up and file them away. They were never used, and were stored shortly after purchase.

The standard fraud on these US bank Mastercards has typically been the false activation scam. A thief will place a sticker with a different barcode over the activation barcode on the back of the card. This sticker will actually be the barcode of a card the scammer has in their possession. The cashier scans the false activation barcode and the scammer’s gift card is loaded instead of yours. By the time you realize your card hasn’t been activated they’ve drained the funds and you’re left having to sort it all out.

Recently there’ve been more cases like mine–the card is not tampered with at all, yet it is somehow compromised after purchase. I’m chalking mine up to sheer volume–when you interact with enough cards you’ll eventually have something like this happen. However it didn’t help that I held these two cards for so long after purchase. It is always best to liquidate as soon after purchase as possible. Fees can be assessed, fraud can happen, and the likelihood of you losing a card are all reasons why liquidation should occur as soon as possible.

In this case I called US Bank and was instructed how to walk through getting a replacement of each card. The process isn’t too much trouble–I have to fax copies of the cards, along with the receipt and a statement about the fraud. I’ll be issued new cards and the fee to replace the cards will be waived.

Good Habits Die Hard

What if I don’t have a copy of the receipt? The phone agent had originally suggested that I return to where I bought the card and ask for a reprint of the receipt. At a major store you should be able to do so–but you’ll need to remember the date and time of the purchase, again something you should be tracking. I was able to access a photo of the receipt on my phone while I was talking with the agent and going over the fraud filing. I take receipt photos in the car in case I misplace hard copy receipts.

Purchase date and time can be obtained in the Milenomics Purchase Tracking system we went over last month. I know it seems like a waste of time to collect so much information, but an example like this fraud shows that when you need it you’ll be glad you have it. Some readers have said they place the full card number in their tracking sheet–in case of a lost or stolen card having the full card number could be the difference between getting your cash back and being out hundreds.

In the end I’m out about 15 minutes of my time ($6.25), but I’m just glad I caught this and had the right record keeping to turn a potential $500 loss into a $6.25 loss.