Today we’ll study up on the subject of Fungiblity of Miles. Simply put–something is fungible if you can exchange individual units for back and forth with each other. The classic example is cash–a $10 and 2 $5 bills are interchangeable. At some point this idea of cash being fungible breaks down . Would you accept 100 $1 bills as change for a $100 bill? You might. What about 1,000 Dimes? maybe not, or 10,000 pennies? There is usually a limit on fungibility. Today we’ll see if miles are fungilble, and if so what limits there are on this fungiblity.

Converting Frequent Flyer Miles: A common question

It is very common for me to be asked by someone how their United miles can be converted to American miles, or something similar. This is because we’re used to booking with money–and money is fungible. This is a classic example of why we need to retain our brain for Milenomics. When we’re just starting out with Miles we think they work just like money–and we assume miles are fungible like money is.

What we come to learn is that miles are not very fungible. Alaska Miles stay with Alaska, United with United. We can book flights with alliance members and partners, this allows us to fly on Alaska with British Airways Avios, or Delta Miles. This is not fungiblity but it does help us to extend the use of our miles.

Most of the time if someone asks can you “convert” miles into another program the answer is no. Today we’ll look deeper at our miles and see if there are ways miles can be fungible, and/or if they can be converted without loss of value.

Refer Back to Credit Card Systems

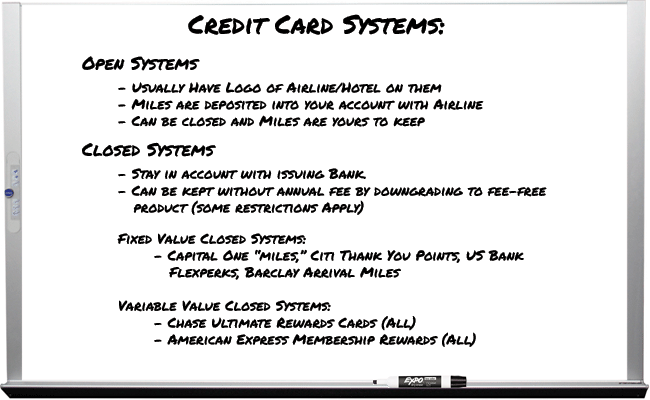

A few months ago I wrote a post titled, “What Happens to My Miles When I Close A Credit Card?” In that post I outline two different types of cards, Open system and Closed System Cards. The Basics were outlined on our whiteboard in that post:

In today’s discussion we’ll be using both of these systems as well.

Open and Closed Systems: Fungibility

With Open System Credit Cards, the miles earned transfer to your personal mileage account at the close of each statement. This is good with respect to closing your card–as you don’t lose any miles, but bad for fungibility. You’re generally stuck with miles in the program you’ve earned them in with these cards. There are two exceptions to this:

SPG Starpoints: These are usually earned one of two ways; by staying at SPG properties, or by spending on the SPG American Express. Starpoints are not only hotel points, but also “convertible” miles. They’ve been created to do this, and it is an advertised benefit of the program. With 30 airline partners these miles can convert from SPG to any number of airline miles. But is this true fungiblity? No because once the miles are in another program they’re now subject to that program’s inflexibility and cannot transfer back out.

Other Hotel Points: We often forget that SPG is a hotel program, and other hotel programs offer a similar “one time” transfer option to airline miles. The difference between SPG and all other programs are that SPG->Airline miles is usually 1:1 or better (with 20k + 5k bonus). Most other Hotel programs, from Hilton to Club Carlson have terrible exchange rates; 10,000 points might convert to only 1,000 airline miles.

Fixed Value Closed systems offer no way to transfer to miles directly, but with Milenomics tricks we can turn these fixed value points into other airline miles.

Variable Value Closed Systems (MR and UR) shadow the above SPG example. You can turn your MR into DL, BA, or any host of other miles. We discussed this when we declared Membership rewards, “Shadow Currency, Orphan Savior and Risky Business.” Ultimate Rewards are the same–they can convert to any number of programs as well.

Again, this isn’t true fungibility because the miles can only be converted within a small group of options, and just as above hotel examples the move is one way only. Once you’ve converted your miles you cannot convert them back.

Buy and Use, instead of Buy and Hold

The lack of fungibility in miles is also an importance consideration when you go to buy miles. If you buy US miles, say during their current promotion, or the one that just passed, you need to use them as US miles. We talked about trying to time the market and buy these miles now, to use them later. The issue with Market timing is that you never know what is coming. And with Miles not being fungible, these two reasons mean we should be very sure we need these miles before we buy them.

The absolute best way to do this is when we can buy them outright and use them on the spot. We could buy a ticket on a flight–and that same ticket could be booked with miles. I’ll use the recent US Airways Gift promo for this example. When a flight is over $660 with US Airways miles and money would be interchangeable for most of us. A good example is around Christmas, or Thanksgiving. You can often book any flight you want for 55,000 miles round trip (with US Airways CC discount).

Assuming you could buy those miles for $.01135 each and then instantly book that flight (which you could) you’d be able to convert money–>miles–>flight on the spot, and save money.

True Fungiblity Will Exist Next Year: AA and US

For a brief period you’ll see true funbility–at least between two mileage currencies. If historical examples are followed you’ll be able to, on the spot, convert 1 US mile to 1 AA mile. And, you’ll be able to convert back, from 1 AA miles to 1 US mile.

This will, while both programs exist, be an example of truly fungible miles. US miles should transfer to AA, and AA to US. I’m basing this on the similar functionality that was implemented post United/Continental merger and post Southwest/Airtran merger. This will, for a while, be an example of two miles which are interchangeable.

Converting Miles to Money

I would argue that the true “holy grail” for most mile collectors is converting from miles directly to money. If Miles could convert easily to money, and then back to miles (through purchasing miles) we’d have much more flexibility with our miles, especially when our travel patterns change, or a program no longer offers us the flights we need.

Can you convert Frequent Flyer Miles to Money? Yes, and no. I’ll tread lightly on this subject, but I won’t toe the line that most do. You absolutely can convert miles to money. Now after a statement that bold I need to add some standard disclaimers:

Your must accept the risks in converting miles to money, most notably your account being shut down, and forfeiture of all the rest of your miles.

You will be dealing with “less than savoury” characters. Think used car salesmen for miles.

Are there people who only apply for credit cards to get the miles and sell them to brokers? Absolutely.

If my travel patterns changed, lets say my wings were clipped and I had to dial back my travel–I’d take the risk and sell at the very least my Membership Rewards points, Delta miles, and my US/AA miles. Chase has been too aggressive in shutting down entire families for me to think about selling UR–especially when Chase will buy them from me for 1 CPP, and I might only get another .5-.8 by selling them to a broker. Not worth the risk in my mind for the extra .5 CPM.

Being EQM-Zero I have much less to lose if my airline account is shut down than someone who’s been earning EQM all year and holds status with the airline.

Trading Miles–Much Better Than Selling Them

Mile trades are a great way to save miles and money. For example–there are some great programs out there, Jetblue, Virgin America–that offer good service, convenient flights, and in seat television. Do you hear much about flights being booked with either online? No. Why is this? I’m not 100% sure. I assume part of it is because the two carriers don’t have very robust route maps. In addition there’s not many good ways to earn their miles. Each has a fixed value type of point, similar to Southwest’s points. But expand your mileage horizons, and keep an eye out for interesting trades. We covered some of this when we discussed MR as a Shadow Currency last month.

Wrap Up

Fungibility is not convertibility, we’ve seen that today. Most of the time something is only fungible if it represents a commodity, like Frozen Concentrated Orange Juice (FCOJ) futures. What we’ve seen today is that Miles are not a commodity. Each program has strengths, and weaknesses, and miles inside the program usually have to stay in that program. Further reinforcing the fact that miles are not commodities is the lack of fungiblity we’ve seen today. I continue to stand by my point that Miles act more like a Non-Durable Good, and today’s post further reinforces that fact.

As for converting miles, we’ve also shown today that the idea is very common, but usually not practical, outside of Variable Value Closed System (MR/UR) and some hotel points. We should also tread lightly when trying to sell miles, and be agressive when trying to trade them. High level stuff, but important to gain all the advantages we can.

Miles are a meant to be used. Hoarding makes Miles sad.

Everything below this line is automatically inserted into this post and is not necessarily endorsed by Milenomics:

I know you like to use the “economics” angle when talking about miles/points, but I think you need to be careful not to stretch too far to make tie-ins because it gets tiring (just one person’s opinion). It’s your niche, I get that, but note that many of us find the “how to” discussions (like booking a trip to Costa Rica) just as valuable as the economic-philosophic discusion.

And did you mean to use the term “Frangibility”?

Blue: I really appreciate the feedback. I’m always trying to better the site, and feedback like this helps. Finding that “sweet spot” between getting the ideas about miles out of my head (lessons) and writing about using miles (bookings) is one target I’m constantly looking for.

I do think today’s post is an important lesson because I am very often asked “why can’t my miles transfer between programs?” While that type of interchangeability would be wonderful it just doesn’t exist in the world of miles, outside the few limited examples outlined in the post. I’ll go ahead and update the tags to make this a #101/#201 post since more seasoned travelers probably already know the details of this.

Chiming in for the other side, I like the economics posts so do keep them coming!

Actually, this post is very timely. Last week you helped me get my son home using 25,000 United miles for a one way Newark-Portland. Expensive, but much better than the nearly $700 that tickets were pricing at when my son suddenly was told he could have enough days off to make it worthwhile to come home for the holidays. He – a 20something who really wants to do it on his own – wants to reimburse me. I told him that someday he could book me a flight or hotel stay. So what’s an appropriate measure?

Looking to give him the best part of this trade, should I ever let it happen, I was thinking that he could:

> book me or my husband a saver ticket using 25,000 miles; or,

> book us hotel rooms that would normally cost between $300-$400

Do you have any other suggestions that would enable him to “pay us back?” He travels a fair amount for work and while he gets to keep the frequent flyer miles, he must take the cheapest flight (within limits) so he can’t focus on one FF program. He does not always keep the hotel miles. (If he travels alone, he can, but if he goes with a group of employees the hotels are normally booked and paid for corporately.) Depending on location, he tries to stay at Hilton where he is Gold, but he does stay at other chains as well.

So what might be a good trade?

BTW, a tip to share that I got from him: He always adds his loyalty number to his hotel record, even if the rate and payment was or will be made by corporate. That can give him access to lounges, late checkout, etc. And sometimes the hotels end up giving him the points anyway. He doesn’t quite understand how it works – whether in theory the points are accumulated by corporate or the rate is low and the deal supposedly means no points – but sometimes he ends up accumulating personal points that way.

Also, because I had the United Explorer card and he didn’t, we used my miles, saving 25,000 in the process as the ticket would have been 50,000! That might make the card a keeper when the fee comes due!

Elaine; I’m impressed your son is taking the booking so seriously. I’m sure you’d let it slide, but he wants to make a gesture of thanks. Apples to Apples would be a 25k booking like you mentioned. But the hotel room sounds like a happy medium–leaving him his airline miles for travel of his own, and something you and your husband can enjoy that otherwise would have to be paid out of pocket. Your first trade, how exciting!

Now the bigger question: why doesn’t your son have the Explorer card? 😉 I recently flew a domestic United flight, something I haven’t done in years since I primarily use UA miles for international travel. By the end of the flight I was surprised the plane wasn’t painted as a giant billboard for the Chase UA MP Visa–the ad was everywhere, in each seat pocket, on the televisions onboard, in ORD; on the terminal monitors, a booth to sign up, posters on the walls, Giant 20′ hanging billboards every 50 feet or so. I literally laughed at how ridiculous it looked. Of course all of those offers were for 30k UA miles on first use (inferior offer), but I’m sure they snag tons of people with those. My point is–make sure he signs up for the full 50k/55k offers before the United/Chase ads bombard his senses and he signs up for less than the max miles. It would pain me to hear he was ensnared by a lesser offer like that!

Much as I try, I cannot get him to sign up for a few more CC cards. He works a lot and travels a lot and feels it is a bother to have to track minimum spends and make sure bills get paid on time. Since I got into this game about a year ago, I have suggested select cards for him, but other than a Hilton Amex he agreed to get when he was traveling 100% of the time, and the REI card he got a while ago, he won’t get any more!

To be fair, he has few expenses and the minimum spends would not be easy for him to do without some MS tricks. When he is on the road for work, they pay all his expenses, and buying VRs or GCs to use with BB is just too much bother for him. He has no college loans and until recently paid no rent. He’s on our family phone plan, and while he does reimburse me for his share, I don’t take CCs 😉 !

I have considered having him make me an authorized signer so I could help him make the minimum spends, but I am new enough at this that I usually have various minimum spends that I am meeting. And living in a state with no CVS stores, I sometimes have to get creative myself.

So, no, he doesn’t have an Explorer card. But it is a good thing both his parents do!