“Sam, the funniest thing happened, I was cleaning my car and I found an old unopened $500 VGC. Hilarious, right?”

No. Not hilarious.

Or maybe you’ve cleaned out a drawer and found a Money Order at the bottom. “Did I ever deposit this? I must have mobile deposited it.”

What if you didn’t?

Enter, Breakage

The standard definition of breakage is basically anything that goes purchased but unused. This is not something most of you think about–but I’m constantly looking to improve any inefficiencies in my system, so I’ve kept an eye on it for a few years now. With respect to our manufacturing miles breakage is the loss of, or forfeiture of any points, miles or money injected into this game.

This means miles that expire, or that you lose as part of AA (Adverse Action), but it also means any money you may have lost. I’ve shared a few breakage type issues on the blog in the past, and similar issues have continued here and there for me. Fortunately the overwhelming majority have turned out to merely be temporary loans, and my real losses have been small amounts.

Estimate Your Breakage Rate

The ability to track my spending using tracking tools has allowed me to also track any and all potential breakage in my system. I’ve estimated my breakage at .017% (0.00017). This means that on a spend of $1000 just 17 cents is breakage. I’ve arrived at this number by taking all real and ‘potential’ losses in a year and dividing by my total spend.

Losses for me are defined as things like cards that haven’t loaded, shutdown and [potential] loss of funds, and even small things like the few cents I leave on some cards (more on that later). I ask you to try to put together your breakage rate as well. It should be extremely close to 0%. If it isn’t you should certainly rethink the entire process you’re using, and possibly put in some techniques that I’ll explain later in this post.

Determine Your Sources of Breakage

Depending on your system for manufacturing miles you might have wildly different sources of breakage. If you do nothing else consider taking an inventory of possible sources of breakage. Your list may or may not include:

- Shutdown of prepaid account

- Leaving pennies on cards

- VGC Fraud/activation issues

- Loss/theft of MO or Gift Cards

- Reasale issues (fraud, spoilage, etc)

- Loss of liquidation method

- Organically spending Visa Gift Cards

My breakage rate has not held steady–it has been as high as .057%. As for why it has trended downward: possibly because of more diligence on my part, but most likely due to potential methods of spending becoming more and more limited. The loss of ‘experimental’ methods and the consolidation around a few proven methods means less breakage overall. My current largest form of breakage comes from buying VGC slightly under $500, a form of opportunity cost breakage.

The issue with breakage is that it is extremely difficult to estimate. By its very definition it shouldn’t be very easy to calculate. So I wouldn’t spend a lot of time estimating it, but I would do it once and try to keep your rate in mind as you go through your spending. Knowing that there’s a possibility of breakage, even if you don’t know your personal rate, is enough to possibly get you using some good techniques to avoid it.

Worth My Time?

Breakage is also an effective way to estimate if something is worth your time. For example I had a situation where $75 was spent in Miami on one of my prepaid cards. I drained the card immediately after. I still to this day have no idea how this happened.

I spent some time (read: a lot of time) dealing with the inept card issuer. They saw that it was loaded in LA and spent the next week in Miami. They investigated and then said the charge was legitimate. In the end I could have pressed the issue, especially because the charge was pushed through as credit. But my time in this situation was already worth more than the $75. Since I drained the card my maximum loss was fixed, and it was an amount of breakage I could absorb over the course of the year easily.

In the end I let it go. I could have spent another hour or two working with this or I could spend that time earning. That doesn’t erase the loss, but it does help me to decide when I jump in or out of a problem, especially a small one.

Best Practices for Reducing Breakage

Stopping breakage before it happens is easy enough if you use some techniques to help track your purchases, and then similarly track your liquidation. When you’re done physical deformation is probably the most useful technique.

Cards: Fold

I’ve covered this here before, and I continue to do this. I will only worry if I find a card that hasn’t been physically deformed. If the card edge has been clipped I know it is at or near enough to $0 that I can consider it dead. This also lets me store my cards without worrying if one with a balance has slipped through the cracks.

I have slightly modified the process from when I first documented it. I now deform the bottom left or bottom right corner, so as to not affect the magnetic stripe, which was actually a tip a reader left in the comments section of the above post. This would be the practice solution to start with, you just fold the corner over right after draining the card.

Money Orders: Encode and Fold

Encoding numbers into purchase prices is something I’ve always done, so it probably comes as no surprise that I advocate doing it with respect to Money Orders. I focus pretty heavily on mobile deposit of money orders. Unfortunately images of the MO aren’t always available online. If I’m auditing deposits for the month end I need to have an effective way to see if a deposit is missing. If one is missing I need to be able to tell which MO that could be. What I do is increment the price of the MO, from .01 to .30 depending on the day of the week. So if I’m buying on Feb 27th my money orders are for $99X.27 (depending on if I use a $499, $498, $497… card).

The second reason I do this is so my purchase is a distinct amount. $999.30, $999.30 $999.30 (or soon to be $999.12) is just too repetitive. If I lose a MO, get mugged in the parking lot, or anything else happens I can go back to the store and say “please look up the purchase of $999.27 money orders from 2/27. There will probably be exactly one transaction at that purchase prices.

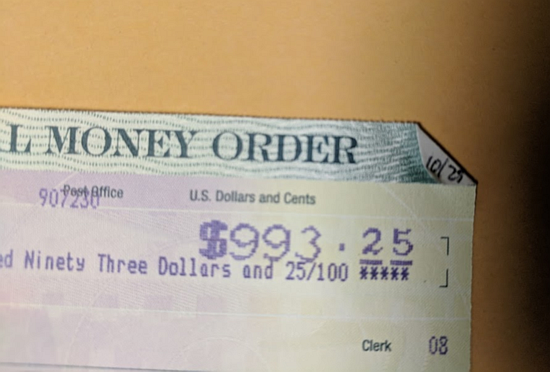

When I deposit the MO I do a similar encoding. I fold over the top right edge of the MO and write the date it was deposited in on the corner. Something like this:

When these are deposited they create distinct deposit amounts tied to specific days. Looking online I can see a deposit of $993.25 was bought on Oct 25th. The folded over corner lets me know I’ve deposited it, a physical deformation that lets me quickly feel at ease when I look at a stack of these. I use this same technique on all checks I deposit actually. This way I know the check has been deposited but I retain the ability to present it physically if there’s an issue.

Points and Miles: Use them

This is an area where significant breakage can happen. Breakage with respect to points and miles happens when airlines devalue and you’ve had your eye on a specific redemption, and that redemption is now out of reach. You transferred 20,000 Starpoints for example, and then the cost of the trip went up in the meantime. Or while you’re waiting for the points to transfer the seats are no longer there.

In addition the expiration of miles and points is another source of breakage. Foreign programs are particularly bad about this, but even domestic programs like UA, AA and yes, Southwest will take your hard earned miles and points. The solution for US carriers is simple–use those points as soon as possible.

—

Any tips and tricks you’d like to share? As I mention above I got one of the most useful tweaks for my physical folding of cards from a reader; I’d love to hear how you limit your breakage as well. And if you’ve never considered any of the above please do give it some thought.

Immediately separate receipts from money orders, tucking the receipts into a different pocket than you will use for the money orders.

Then write your name in and sign the money orders before leaving the premises, rendering them useless to anyone but you. Carry a pen if you have to.

Should you be mugged, hand over the money orders, but keep the receipts. You can call MG or WU on the spot give them the receipt numbers and block the money orders from being deposited by anyone else.

Yes! I endorse them “For Deposit Only” to hopefully further restrict them. Agree that carrying your own pen is a smart move too.

“FOR [[X BANK]] deposit only” should really limit someone’s options.

Oooh,, really nice!!!

I’m sure my system sounds equally silly to you, as your’s does to me. But in summary I don’t bother with card folds, MO cost codes, or such.

When liquidating, I wrap MOs around the associated GCs, and keep them around a single rubber band. Once a month I check the balance of GCs from 3 months prior, verify the deposit of the associated MO and then dispose of them all. I keep a detailed spreadsheet which provides an auditable trail from purchase with to MO liquidation, should anyone ask. Nice, simple and efficient. At least to me 🙂

Radster: doesn’t sound silly at all. This post (and most here) are about sharing what works for each of us so we can work out how to become the best individual ‘us’ possible. I like the ideas you laid out here, and think readers can learn a lot from your system.