While Friday’s post about purchase tracking is applicable to all of us, today’s is going to be much more subjective. What works for me may not work well for you. And what works for you may not work well for anyone else. Finances are tricky for some of us to figure out–so today I’m going to give you some general tips on how to ensure you pay all your bills on time, and earn your points and miles without paying the banks any late fees.

If You Don’t Trust Yourself–Scale it Back

I’ve mentioned this before; but if you cannot pay your credit card bills in full each month then this is not the game for you. If you do find yourself struggling to make ends meet, you could switch energy providers to cut back on utility bills. Additionally, remember the float rule–which states that If tomorrow your ability to cash out MMR purchases went away would you have serious issues with paying your credit card bill? If the answer to that question is yes–you should scale things back a bit.

Another good piece of advice is to have a well set up system of accounts. At the most extreme keep all your “real” spending on a single card or even a debit card. This means your MMR’s should always balance neatly at the end of the month. If they don’t then something is wrong. Today’s post relates back to the Financial Firewall we discussed a few months ago–and also helps to keep your system of accounts as un-complicated as possible. Having a spare checking account to keep your real finances from your fake finances isn’t just a good firewall, it could mean never missing a payment, or coming up short.

And finally, Milenomics is different–we’re going to plan out the miles we need, using a demand schedule, and then earn up to those amounts, booking as we go. When we’ve hit our targets we’ll either switch to cash back cards, or scale back our manufacturing operations.

Repetition, Repetition, Repetition…

I’m a creature of habit. My habit is to check my activity on my cards, sometimes as often as daily. I log in, check the purchases and then log out. My cards fall into 5 major banks: Citi, Chase, Barclay, Amex, and FIA (Fido Amex’s). Logging into these and checking the accounts allows me to know the due dates for these cards, make sure the last month’s payment has posted correctly, and also verify purchases.

I also pay my accounts directly on the card issuer’s site. I’m not a big fan of “pushing” payments from my bank to the card, I’d much rather pull them from the card issuer’s site. The danger I see in paying direct from my checking account and never logging into the cards issuers’ site would be that something went wrong and the payment didn’t post. I’ve had that happen–Sending a Bluebird payment, and the payment not going through.

Alert! Alert! Alert!

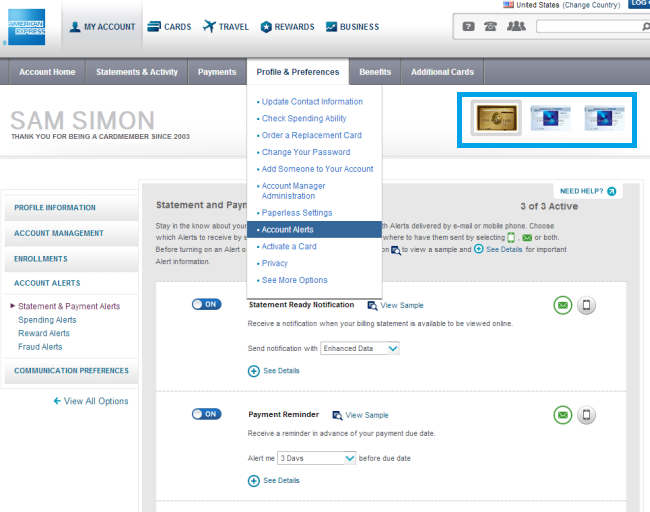

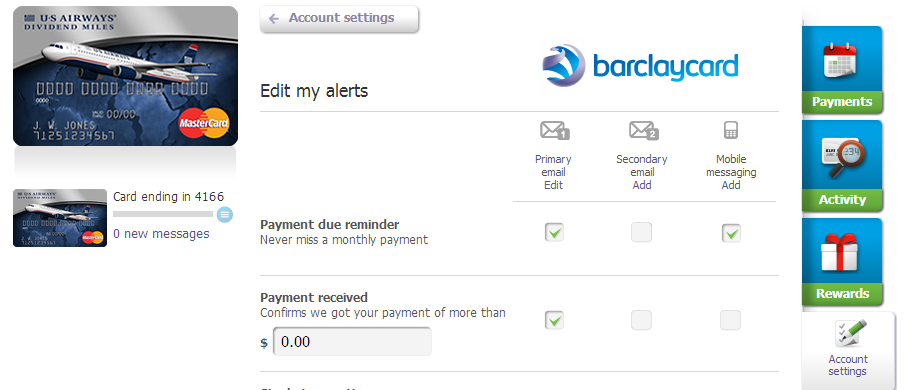

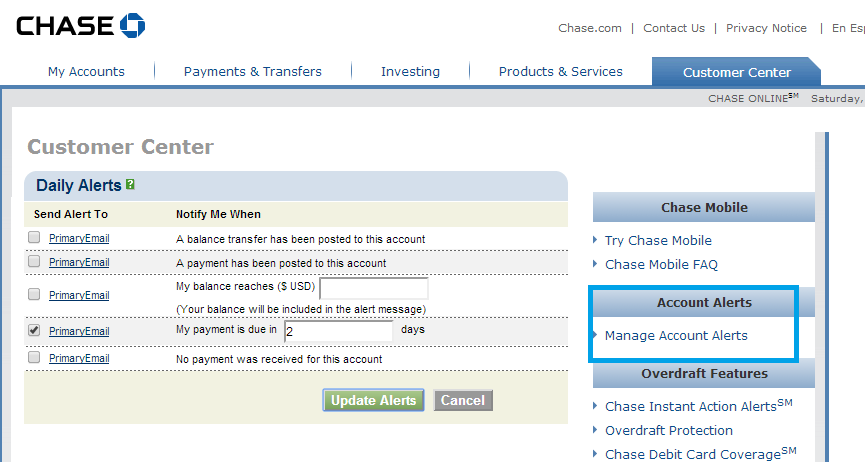

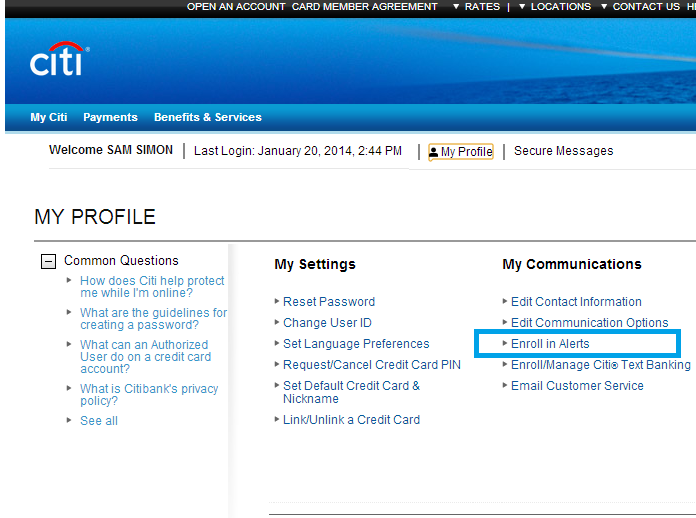

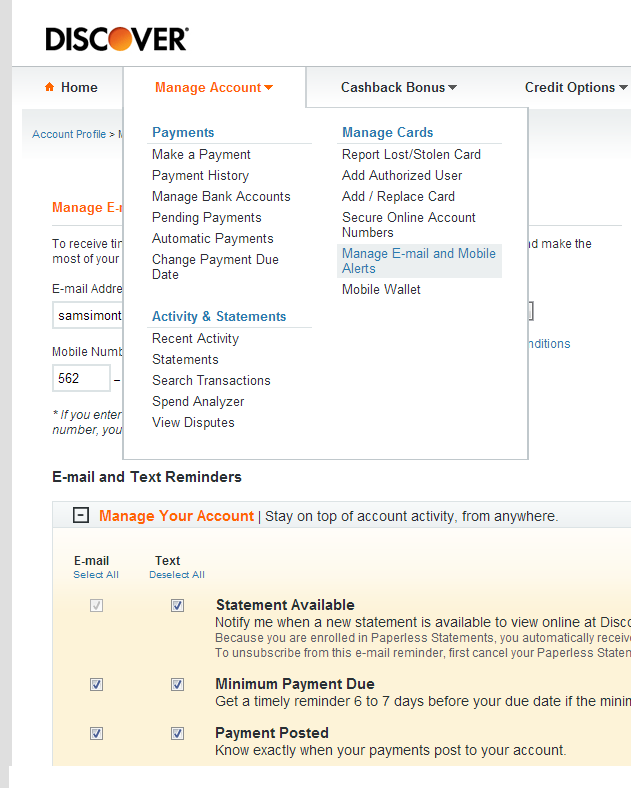

Almost all banks allow you to set up payment reminders. Set these reminders. I like to set them for a worst case scenario–I forgot totally about a card, haven’t logged in all month and a charge hits the card and I don’t realize it needs to be paid. This is especially important for those accounts I rarely use, as I’m less likely to constantly log in when the balance is $0. Doing this takes only a few minutes per card, and only needs to be done once for the life of the card. Some examples of these alerts are:

American Express

Barclay Bank

Chase Bank

CitiCards

Discover Card

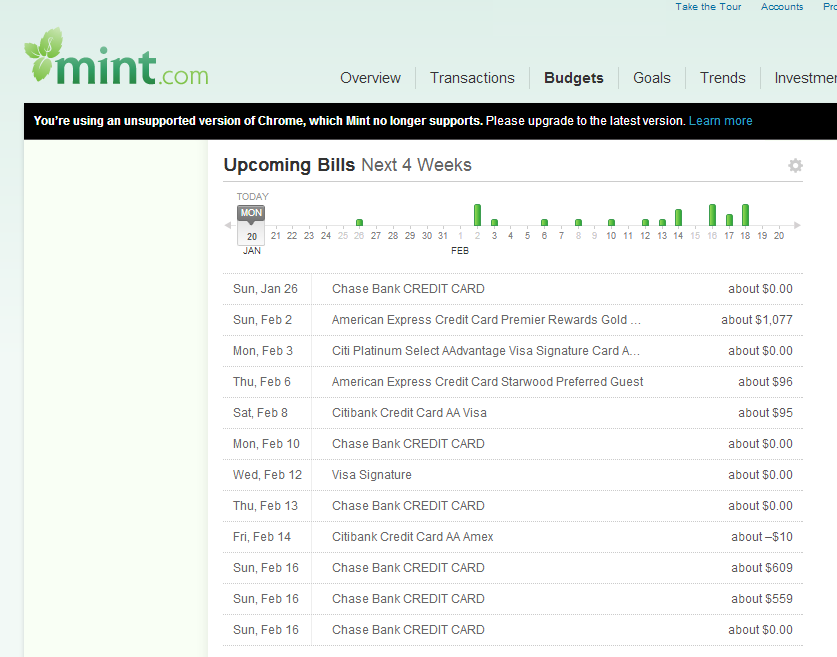

Using Mint.com For payment Reminders.

As outlined in this excellent comment by Robert mint.com is a great service to use for budgeting and keeping track of payments. The good part about Mint.com is that when you have a bank already set up with mint, new cards are automatically added to your mint.com and tracked for purchases and due dates.

For me Mint.com is great because it funnels all the payment alerts to my email. My wife’s cards are all set up to send payment alerts and such to her email address. In Mint, I’ve added her cards so we have one universal budget. An added benefit is that I can keep track of all of our bills in one place.

Right when you log in you’re shown your upcoming bills:

You cannot pay bills from Mint.com. For that you’ll need to either set up bill pay at your bank’s site, or pay direct on the card issuer’s site. Mint.com is great to really keep an eye on spending and payments, especiallly for a Dual Earn Dual Burn type of family.

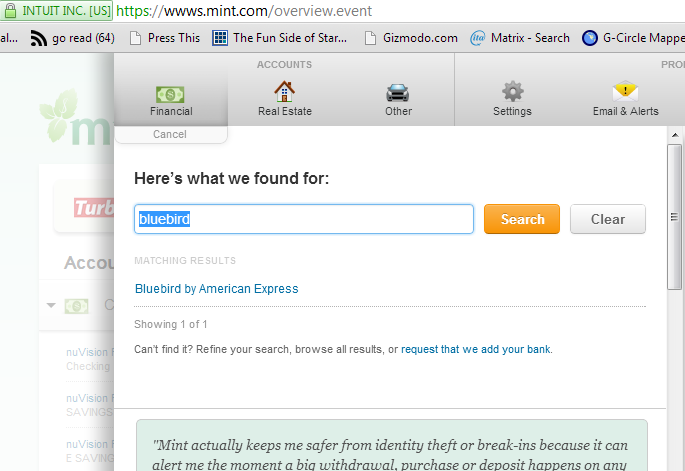

Adding Bluebird to Mint.com

Adding your Bluebird (or Serve) account to Mint.com is easy, and a great way to keep track of your BB Purchases, Checks, deposits, and such. Simply add a new account and search for Bluebird or Serve. Using mint.com to keep track of multiple bluebird accounts is a great way to keep everything in one place:

I create a budget for Bluebird–and all my Bluebird activitiy I code with “Bluebird.” At the end of the month this budgeting item should balance out to near $0, with whatever is left being the fees paid for any purchases.

Note: The last half of this post includes some #RiskyBusiness, caution should be used:

When Float Becomes (even more) Valuable Again

Some of you will not want to read this section. For those of you who have been known to miss a payment date, or have a very tight cash reserve, paying your bill when you receive it, rather than when it is due could be your best bet. For those who are more adventurous there are benefits to be had from using the float off your credit card.

Right now there isn’t as much incentive to pay your balance as close as possible to the due date. In fact some would argue that allowing the charges to even post on your bill or make it on the bill will hurt your credit score (due to % utilization). All of this is true, and should be considered.

The exception to all of this is if you’re using your credit cards as an equity line and making money (and miles) off of the float. If you’re doing that you’ll likely want to keep the money moving as long as possible, and that means paying as close to the due date as you can. I’ll challenge you to build good habits now, while interest rates are at or near 0%, and be ready for the future should interest rates ever rise again.

Even right now, Look into opening at least one High Interest Rewards Checking Account. There are some with rates as high as 4%, and limits of $20,000 for that 4%. You could even open an account that pays you in AA miles instead of interest (fees apply). Finding a Rewards Checking account which allows you to put $20k into the account and earn 2.5% on that account would mean you could do something like this:

Purchase $20k in financial products each month. Cash these out through whatever means necessary, and deposit the cash from these $20k worth of products into the rewards checking account. Hold the cash in the account as long as possible, while simultaneously re-buying the same products each month. You should have periods where you overlap, and more than $20k is in the account, which is fine. As your due dates come near, pay off the first month’s purchases with the Rewards Checking account.

You’ll continue to rotate money into and out of this account, and your average daily balance should always be at or above $20k. You’ll pocket the $42 or so in interest each month. You will owe tax on this $500 a year, but can still be used to offset fees. This account could be shut down--so it should be firewalled from your regular accounts.

If reading the above makes your head hurt–then this type of churning is not for you. This is the type of setup I alluded to when I challenged you to create a MMR method without buying any VR. Finding purchases that cut your costs as much as possible, and then loading these up into an account that pays you back are two great steps to reducing your Cost Per mile.

In the above example you’d earn 20,000 – 40,000 miles per month (with a mix of 1x and 2x cards), and could either use the float to generate more DL/AA/AS miles, or take the interest payment from a High Yield Checking Account instead.

Again, this type of coordination is not for everyone. Doing this means you’re now balancing two sets of books, your real finances, and your “shadow finances.” Keeping these two areas totally separate is very important. Fooling yourself into thinking your shadow money is yours to spend is a great way to end up in financial ruin.

Wrap-Up

I wish I had a foolproof way for all of us to make sure we pay all our bills on time. For me the solution is to make checking these things part of my daily routines, and creating a plan which involves multiple fail-safes in case I forget about a bill or an account.

Depending on your bills, your cash reserves, and your preferred payment methods some of the above tips may work well for you. Others may not. Finding your way, and creating the best system for you is what Milenomics strives to achieve. If you don’t trust Mint.com with your bank login, and I know some of you won’t, then skip it, and rely on alerts from your bank.

If you’re like me, having one set of alerts is good, but having a second is better. Set up those alerts, and make sure to pay those bills on time, every time. In the meantime consider a system of accounts, and look at ways in which you can extend the life of your churn to earn more miles and money along the way.

Everything below this line is Automatically inserted into this post and not necessarily endorsed by Milenomics:

Am I missing something or isn’t it 2000 – 4000 AA miles a month, not 20K – 40K? Clicking through to the BankDirect site says

Earn 100 AAdvantage® miles per month for every $1,000 of the average daily collected balance in your Mileage Checking with Interest Account up to the first $50,000 on deposit. For average daily collected balances over $50,000, earn 25 AAdvantage miles per $1,000 on deposit.

Or am I missing something?

PWAC: I probably wasn’t clear enough in the wording of the post. The $20k in spending per month generates the 20-40k in miles per month.

The BankDirect AA miles would be in addition to this, basically a 10% bonus. Your math is right, just 2,000/mo for a $20k avg. daily deposit. They’re also charging a monthly fee for this account–so the value isn’t great, but I wanted to include it in the discussion.

Or you could take the interest payment on that deposit, $42 a month or so. ($500/yr)

Or use it with a mile earning debit card to leverage further (20k-80k more miles per month).

All three options are complex, and juggling like that isn’t for everyone.