Today we’re back on the Risky Business topic, with an offer for using what we know to step up to the next level. Absolutely not #101 level stuff here, so if any of the following doesn’t make sense it probably isn’t a good idea to try it out. This is also a bit of a fantasy post at this time. I’ll explain why later, but I think doing something like this is about 6-12 months off into the future. Still always good to be prepared.

If you’re anything like me you often get applications (and sometimes pre-approvals) for cards that stink. I mean really terrible offers. I’m sure you get them too, and you don’t give them a second though, tossing them into the shredder. You know the type; really useless (and not just use-less) kind of cards. 1% rewards, nothing special, no real benefits, no sign up bonus. But they come in all the time.

Sidebar: If you haven’t read Robert’s piece on the ways to unlock more sign up bonuses please do, it is EXCELLENT. He outlines the problem many of us have reached–as you apply for more and more cards you reach an outer limit of low hanging fruit.

Back to the topic at hand. Today I’ll go over an offer I received, why I am considering it, and how the bank should be pitching the offer to make it more enticing.

The Offer:

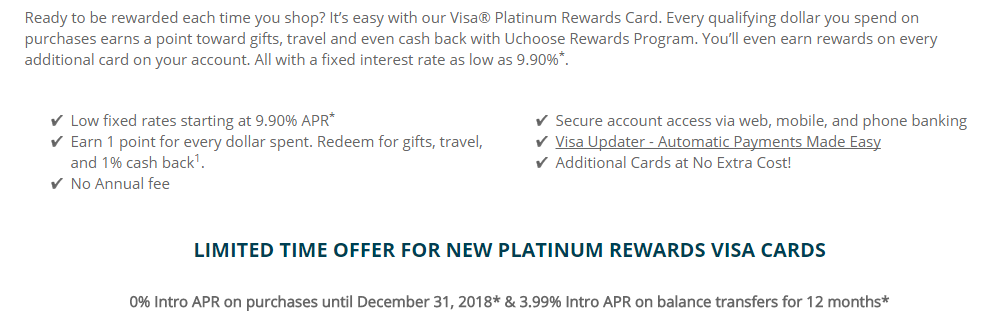

I get 1-2 of these types of offers a month. Small banks, or Credit unions send these out hopful I’ll take a leap. There isn’t a sign up bonus for these cards and they don’t earn well. I usually trash them. But lately I’ve been chasing ever higher hanging fruit, so I started to open and at least consider them. The above offer was sent to me as a pre-approved $15,000 line. This Credit Union does send actual Pre-Approvals which you can accept and no hard pull will ever be done.

The details of the offer are in the image above. The card is nothing spectacular, earning is 1%, but the kicker is the “LIMITED TIME OFFER,” of a 0% BT or 0% on all purchases. The BT offer is not a true 0% offer–it is actually a 3% fee, up to a maximum of $100. For my $15,000 credit line this would effectively be a 0.6% BT Fee. That’s not terrible, but most cards don’t cap this 3%, and so you’re stuck with a relatively low interest loan but not a 0% interest loan.

But Wait…There’s More!

So lets take what we already know and extend it outward, using the ideas of manufacturing miles and points to manufacture money out of thin air. Let’s say I take this offer. Great! I’ve got $15,000 I can spend. But… I only earn at 1%, and there’s no spread on these points–they’re worth 1cpp (or less). And I already have the best cash back cards on earth…

But this is a really, really low interest loan. Almost no interest. And we’ve all become exceptional at cashing out our credit limit and paying that money back. So let’s do that here, except instead of paying the CC back before the statement cuts let’s pay it back a little later–say 12 months later. After all, the bank is telling us we have all year to pay them back.

My average costs to earn and liquidate $1,000 are about $12+T. So to do $15,000 I’m looking at $180 + My Time. The Card earns 1% back, so the rewards would take -$150 from this and I”m left with $30 OOP + the time to buy/liquadate $15,000.

My Time to do this is worth more than $70.

For the above card, with a cap of $100 on the BT I’d just BT the full amount and eat the $100. But I like to open cards like this in groups, so the same idea of buying and liquidating would be one I could use for another 0% purchase offer that doesn’t cap the BT.

So now I’m sitting on money that’s not really mine, but costs me <.6% to hold. Great you’re thinking… now what? I haven’t earned a single Mile, or point and I’m actually negative $30-$100 + some time.

Add a High Interest Account to the Mix

This is where the twist comes in. I mention this fact in my 2018 Crystal Ball post; But the App-O-Rama (AOR) was never about signing up for huge credit card sign up bonuses. From the start it was about these 0% BT offers, and parking that money into higher interest accounts. Most of you will remember that Charles Schwab was (at a time) paying 4.25% on their checking account (It now pays a paltry .15%).

You could take 0% money, hold it in a 4.25% account, return the money to the CC when you’re done and pocket the difference.

Or use the funds for Checking account bonuses that would otherwise be out of reach.

This is [almost] free money, so let it flow into low risk (or no risk) and High interest reward type accounts. I don’t recommend doing any of this if you can’t be trusted with large sums of money. If you’re tempted to use it to buy BTC, stocks, put it all on Red and let it ride, stop, do not do this. Also if you or your kids are applying for financial aid soon this might be a bad time to have large deposit accounts.

Do 4.25% Accounts Still Exist?

These aren’t exactly the same as an old Schwab High Interest Checking account. There are hoops to jump to get these higher interest rates in our current low interest rate economy. Today’s discussion is more academic than practical right now. So we’ll have to wait for more standard account rates to rise, or decide if jumping through the hoops with high interest accounts are worth it right now.

The highest you’ll get without any hoops would be something like a 1 year CD at around 1.95%. That’s a spread that’s just too thin right now when you consider that in addition to time, fees, and travel you have one other big ‘cost’ associated with this type of activity:

Your Credit Score Will Take a Hit

Longtime readers of Milenomics know that I’m leaving out an important 4th area that this offer ‘costs,’ and that is your credit score. Time, Travel, Fees, and Credit score are all going to be things you’ll need to put into this to make it work.

When you open a new card and max it out you’ll see a ding on your credit score. A pretty significant ding. Especially if you keep that utilization way up there. Ideally you’d do an AOR of these types of offers and get as much credit as possible, float it for the 12 months and then pay everything off, let your score recover and do it again. This income is taxable, so the net to you is a bit lower still.

Consider not using the entire CL, and instead doing 66% of the lines. For my above $15,000 offer if I did a $10,000 in the above account I’d still earn $450. $450 for $10,000 in spending…That’s not too shabby. This leads me to my next point: These offers are being pitched incorrectly.

Rethink the Offer

If anyone here works for one of these banks please send the marketing department the next paragraph:

The issue with these cards is that the banks who make the cards don’t market them right. They downplay their biggest benefit (0% for X Months), and play up weak benefits like 1% earning. If I was in charge of marketing these I’d downplay the crappy earning and in HUGE letters talk about how there’s a potential $450 cash bonus when you spend $10,000 on the card (And put that $10,000 in a high interest account). Now how does this card seem?

I don’t think we’re exactly at the right time for these kinds of offers, but we’re closer than we’ve been in the last 5+ years. Interest rates need to climb a bit more for these to become a reality. A nice 12-month CD earning 3.5% would be ideal, and easier than the hoops you need to jump through with High interest Reward checking. While we await those higher rates be ready to add this to your arsenal.

Everything old is new again.

Did this about 10+ years ago with combined $250K in 0% loans.

True 0% $0 fee balance transfers and 5,6,7% interest rates IIRC.

Hope they do come back but we still have quite a ways to go.

Rick: Would love to have gotten in on things then, alas I was a lowly college student at the time.

Interesting development now is that for whatever credit lines you currently churn you could theoretically open a CD worth (CL/2). Manufacture up to the credit limit on half the cards and deposit that money into the CD. The next month manufacture on the other half of the lines and pay off the first lines, then keep doing this month after month until the CD matures. Lather, rinse, repeat.

Of course we need those 5-6-7% rates for it to be worthwhile, but still something to consider in the future.

Interesting idea. We just put the 0 transfer proceeds in the interest bearing account and had automatic minimum payments set up until the end of the 0% interest rate period. Between wife and I, we had $250k at 0% and a nice income stream. Longest ones were 18 months.

Never considered cd’s