Today I’ll introduce some of you to what I think is the best Cash Back credit card on Earth. “Best on Earth” is a bold statement to make, but one I’m confident I can back up. For those of you unfamiliar with it, today we’ll be discussing this card:

The Fidelity Investment Rewards American Express.

Just because you don’t hear a lot about this card don’t discredit it. Remember, money talks–and lots of other cards pay people to talk about them. Fidelity doesn’t, and because of this you hear relatively little about it. I’ll go over when and why using the card is so beneficial, and then talk about ways to compound the rewards to earn even more off of this card.

There hasn’t usually been a sign up bonus for this card, but that has recently changed, and now you’re offered $75 when spending $500 in the first 60 days. Yes, I know not much of a bonus–but there are many reasons I suggest everyone have this card, and even without the $75 sign up bonus I’d still recommend it.

A, B, C; A-Always B-Be C-Charging

Anywhere you’re not earning large category bonuses the Fidelity Amex is almost guaranteed to be your best card to use. It can also be useful to generate cash back from time to time for purchases of Amex GC or other items online with low/negative fees.

Personally, I use mine as a hedge against holding the over-rated Chase Sapphire Preferred. Anywhere the CSP is offering 2x UR this card is also offering 2 points per dollar. Anywhere the CSP is only offering 1 UR this card is still offering 2 points per dollar.

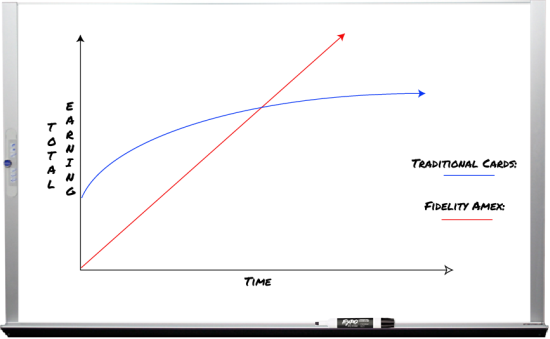

2% back with $0 Annual fee compares to no other card out there. The 2% rewards with this card are unlimited and come with no annual fee. While you’ll find other cards with promotional rates higher than this card, nothing matches it for day in, day out, cash back. There are even some deals which only work on this card–and those alone could net you $2,000+ in cash back per year, per card.

I’ll ask you to think of this card differently from other cards. With most cards you apply, and receive a large bonus upfront. After the first year is up your bonus is eaten away by Annual fees and you start to earn rewards more slowly. This card starts off consistent and keeps earning at the same rate:

The deals which can net you $2,000 this year can do the same next year, and for as long as those deals continue. What that means is this card is a keeper, and is always near the front of my wallet.

Rewards that Compound (Or, Turning This into a 3% cash back card)

The Investment Rewards card earns “points,” each of which is worth 1 cent when credited to any of the following accounts:

- Cash Management Account

- Brokerage account

- Fidelity-managed 529 account

- Retirement account

The points transfer 1=1¢ into these accounts, and can be transferred out from some of the above accounts. Today we’ll talk about keeping them in a retirement account, and using that to increase our cash back by as much as 50%.

We’ve talked about fiscal responsibility a little here on Milenomics, but for serious discussions I recommend Matt’s blog over at www.saverocity.com. Matt and the guys at all the Saverocity blogs have probably covered this card more than all other sites online combined, and he’s written some great advice on how to use the card.

Pay particular attention to this post, and the comments, where Matt and I discuss using the card to open and fund a retirement account. For anyone who qualifies for the Saver’s Tax Credit the cash you put into your IRA with this card can be matched by the US government up to 50% (of your first $2k). What this means is that if you fall into the 50% match category your first $100,000 spent on the card will be earning you 3%. The saver’s credit goes all the way from 50% down to just 10%. Even at a 10% Saver’s Credit you’re still looking at a 2.2% earning card.

It isn’t often that using a credit card can help you in the long term–but this one certainly can. With years and years of compounding your $2k per year, enhanced by the Saver’s credit, can grow quite a bit. Fidelity has a calculator for seeing just how much your yearly spending could turn into, located here.

Granted this is a benefit of any card which earns cash back, so long as you choose to put that cash into a retirement account. I bring it up to ask you to consider the long term financial health of starting a retirement account and using this card as a vehicle to fund it. If you already save towards a retirement account, or if you don’t qualify for the Saver’s credit then this “bonus” 1% doesn’t apply to you.

Amex Acceptance Rates

Usually in discussing this card a blog will add a disclaimer of the sort; “This is an American Express Card, which isn’t as widely accepted as Visa/MC.” I find it a bit unfair to ding this card for being an Amex, but push an Amex Gold/Platinum without a similar disclaimer.

Yes, I’ve found the occasional place that won’t accept Amex–but that certainly shouldn’t dissuade you from applying for this card. My personal belief is that the Amex acceptance argument is a way to steer people towards something like the Barclaycard Arrival World MC, which I feel is an inferior card (long-term) to this Fidelity Amex.

Visa/Mastercards Can Be Inferior As Well

I’ll channel Ronald Reagan here and say, “I will not make acceptance rates an issue in this campaign. I am not going to exploit, for political purposes, Visa/MasterCard’s inability to qualify for Amex Sync Deals.”

In response to the argument that this card is an American Express card, and won’t be accepted in as many places I’ve decided to argue that this card is better than a Visa or Mastercard, and is accepted in numerous money saving ways that Visa/MC are not. This card can be Sync’d with Twitter/Facebook and used for Amex deals. It can also be used on Small business Saturday. There are also deals to be purchased online which only work with this card, and cannot be bought with Visa/MCs.

I hope to change the discussion on this card–from one of “This Amex isnt’ accepted everywhere Visa/MC are,” to a discussion based on the true merits of the card. Obvioiusly, I’m a huge fan of this card, and want to spread the word about it to all who will listen.

Double Dipping Via Bill Payment

Free-Quent Flyer reported this last week that this card is now the only one of just a few Amex cards which can be paid at Wal-Mart Money Centers using their bill pay option. For more information on which cards are payable and how to do so, consult this Flyertalk thread. This opens the Fidelity Amex up to double, triple, or quadruple dipping–charging up this card, and then paying it off to earn even more miles. This is a strategy which doesn’t work for even the big name Amex’s: The Gold PRG, or the Platinum Amex.

Employing a mile earning debit card, and this Fidelity card are surefire ways to earn big miles, at almost no cost besides your time and travel.

Special thanks to Flyertalker CreditPig as well as MsArbi for testing and reporting their success in paying this card. Also a H/T to HikerT in the comments for pointing out my error in not crediting these two for their hard work in figuring out how to pay this card.

The King of the Ring

Add it all up; $2,000+ a year in cash back on deals that only work on this card, up to 3% back if you claim a saver’s credit, Bill Payment which saves you from having to lug MO’s around town, and this card is unmatched by any other cash back/travel “points” cards out there.

If you have an idea of a card to put up against this one–let me know. I’m all ears, and love a good shootout between credit cards. If you’d like to try to find fault in the Fidelity Amex I’m all ears as well, and think that readers will benefit from a healthy discussion of the card’s positives and negatives.

It’s strange that you can’t do Walmart Bill Pay to credit cards issued by Amex. Do you have any speculations about what the reason is? My guess is that Amex doesn’t want to go through the trouble of making their credit cards compatible with Walmart Bill Pay, and they don’t think it’s worth the cost of implementing it.

Also, what about other cards that use the Amex payment network but aren’t issued by Amex, such as the Bank of America Virgin Atlantic Amex or the Citi AAdvantage Amex? Can you do Walmart Bill Pay for those?

I do think this Fidelity Amex card is a great credit card. However, it’s a stretch to say it’s not a well-known credit card.

Brandon: Pure speculation: but All Amex cards worked until around Jan. of this year. Either Amex pulled out or WM updated their checkfree to exclude Amex (possibly due to $$$ dispute?).

Citi AA Amex doesn’t work–But I don’t know about another BofA Amex–good point there. Would like to know if anyone has positive experience with the card. I’ve toned down the post title after your comment–you’re right, it is pretty well known, just not talked about enough, and I want to start a conversation about it.

Are you sure the Citi AA Amex doesn’t work? If you go to the original source and read the wiki at FT you would see the Citi AA Amex is still reported to be payable. Just one example of why it’s bad practice to credit bloggers for “reporting” things when they aren’t the original source. At least FQF cited the original source.

HikerT: I appreciate the feedback. Not crediting the orginal source(s) was an oversight on my part. I take my crediting and linking seriously, and have gone through and updated that section of the post with better info, and links. I’ve also reworded the section to show that other Amex cards are payable as well.

I don’t have this card mostly due to the low sign-up bonus, but it is on my list of cards to get someday. I’ll get it once I run out of cards to apply for, which with Chase is not too far off. Disney Visa, here I come! 🙂

I could be wrong, but I thought it doesn’t qualify for Amex promotions, because it’s issued by Bank of America. Maybe someone can chime in.

As far as other cards to consider, it depends on your spending level. Amex Blue Cash Preferred and Amex Everyday Preferred as well as Sallie Mae Barclaycard could easily trump the Fido card for low spenders. That is people who put around 24K yearly on credit cards.

How about this: if you get it email me and we can discuss strategies for using it? 🙂 I’ll work to convert you to the green side! Amex promotions which are added directly in your card won’t work with this, since you don’t log into an americanexpress.com account. Twitter and Facebook Sync deals should work ok for this card however.

Those strategies wouldn’t happen to evolve… err, involve gas stations and grocery stores by any chance? 🙂 Interesting to know about Fido card, makes me want it even more.

Oh, and thanks for beating up on CSP card. I will make it my mission to convince everyone that it’s overrated. Punk on!

Leana: They do not actually–this card is a bit of an oddball really; for gas/groceries/drugstores there are much better cards, and therefore it doesn’t see a ton of play in physical stores for me. Wherever there *isn’t* a large category bonus it comes out to play. Some of that is legit spending (which pales in comparison to non-legit spending, but still is important to earn from). The real fun with this card occurs with some online deals and such which only work for this card. I like making money from the comfort of my home/work, and this card helps with that for sure.

Thanks for clarifying, I thought you meant something else. I’ve sent you an email. I’m always interested in ways to make money without shlepping to various stores. With my kids, I dread going in public, as there is inevitably a meltdown awaiting.

Might I be cheeky and take you up on your offer to leana to email you to discuss strategies for using this card? I recently was approved and have a few in mind, but would love your thoughts.

Also, this might be a useful data point for some people who want to apply for the card – if you have only a couple of years of credit history the application seems to be automatically denied. Well at least this happened to me twice, even though I have excellent credit. The first denial I couldn’t get through to a human who could assist me, but with the second I tried multiple numbers listed, most no longer active, and finally spoke to someone who was able to reverse the decision really quickly and easily. So, if your credit history is solid and you get a denial, the reconsideration line is great at reversing this with a quick review of your file and a few questions.

The only reconsideration number I found that worked was the dedicated Spanish line, but there was no issue with me only being able to speak English. The number is 1-866-865-7843.

GirlMeetsWorld: Thanks for the tip about reconsideration numbers!

As for the cheeky-ness, the most I’ll say about it publicly is this: http://saverocity.com/travel/pay-75-100-month/

Thanks – I was in touch with Matt about that last year. Thank-you for the reminder, much appreciated. This is a great post. Thank-you.

I’ve talked with Matt about his unique angle on this card and can’t get over the fact it involved large sums of money sent through the mail without any tracking or delivery confirmation. I also don’t like that once deposited it might arouse AML suspicions. What are your thoughts on this?

Smitty: there are always risks. Think about leaving Wal-Mart with $4k in money orders… Or people noticing you come in with gift cards and load bluebird every time for $1k…high risk maneuvers abound in this game. You could be mugged leaving CVS by the guy/gal behind you in line who overheard the cashier’s loud “your total is $5,000!”

For me the risk is actually not that high. You’re told when they ship, and if they were stolen whoever took them would then be looking at mail fraud as well as bank fraud.

Fraudulent Use of them is more traceable than stolen gift cards would be, and they can be canceled and reissued if lost or stolen.

There are risks, but if you’re truly not buying them because of the risks you may want to analyze the true risks in other areas of your churn…I think you’ll find similar levels of risk abound. No risk… No reward.

As for Aml issues… There’s always a risk of suspicion. Money orders are risky in this way too. I’m not a lawyer so I can’t speak to the legal issues, but I keep a paper trail just in case.

I am planning to apply for this card next month. Would you also share with me strategies for using it?

It isn’t just WalMart that stopped accepting AmEx BP it appears to have been the entire CFP network.

With our refi successfully completed this past Monday, this card is top of my list for our next churn. But I am postponing it until after the CLT DO, in case I hear about any cards/offers there to include in that churn. Meanwhile, I am using the Arrivals card for most non-bonus spend, but that will end at annual fee time.

BTW, I got a targeted email offer from Barclays to spend $750/a month in May, June and July to get 15,000 points. It is my second such offer while my poor husband hasn’t been targeted even once! I remain baffled by the vagaries of such offers. But at least one of us got it.

Also got an easy 1000 points when I received the Priority Club/IHG new Mastercard that replaced their Visa – any easy one swipe for 1000 points.

Thanks for this post. I look forward to exploring some of the ways your mention to make the Fidelity card more lucrative.

You received a 15k point bonus?? Mine was the same offer only it was for 5k bonus points! Not fair

This card does get a lot of coverage outside of the points & miles space, it was given the best credit card by CNN money.

Really solid article, carefully explained. The underlying premise is asking oneself “Why am I doing this (eg. Using a miles-earning card). In some cases, one should not and those cases are becoming more and more prevalent as devaluations erode FF program benefits.

The reason the points and miles crowd doesn’t write about cash back more is that cash back cards generally do not pay a referral commission to the writers who hawk the cards and provide links to applications for them. Everyone should decide if you’re reading something designed to give you good advice or something designed to sell you something.

One further benefit of Amex-it is the only card accepted at Costco, which often also has the cheapest gas.

I am confused by your comment “Pay particular attention to this post, and the comments, where Matt and I discuss using the card to open and fund a retirement account.” The linked post says that there are 6 comments, but I can only see two comments, one from Matt and one from TV. Are there hidden posts from you that I am not seeing or is the link wrong?

Thanks for pointing that out Kim. I linked to an incorrect post, the link should have been:http://saverocity.com/finance/fail-5000-brokerage-account-december-edition/ I’ll also update the post.

There’s also the Capital One 2% Spark business card that rarely gets mentioned. The crappy thing about Cap 1 is they (supposedly) pull 3 credit reports (one from each major bureau).

FWIW, I don’t put any of my $250+K/mo MS on 2% cash back cards – get more value out of miles/points for premium travel while also generating meaningful cb using portals and better cb cards.

As for the 3% Savers Credit, your income has to be paltry to qualify. If you are spending time fooling around with 2% cb and you qualify for the 50% bracket, you’ve got your priorities vastly out of whack. Time to get educated and a decent job.

Couldn’t disagree with you more. Why not use the card for MS while getting the education? What kind of jobs do you think young college kids can get? Or is daddy big bucks paying for everything?

My son/DIL are earning $2K/month doing MS which is a great supplement to their income while they attend college. It basically adds 50% to their income and it is far less effort than their regular jobs.

Lets see, which is easier. 10 trips to WM and CVS a month or work another 150 hours/month?

In fact I would argue MS can be more suited to the lower income individuals because they earn less per hour on their regular jobs. So as long as they have good credit and a good enough CL, which I have helped them to attain through good management and applications, this MS is a great way to earn greatly needed cash as well as miles.

They are doing $2K in cb a month on a 2% Fido card?? I say total BS! After cash out fees (of ~1+%), that means they are doing in excess of $200K a month volume.

I couldn’t agree with you more on your point about AMEX not being accepted everywhere as an excuse to choose the VISA/MC version over the AMEX. In my personal experience, the only places that do not accept AMEX either don’t except CCs at all (i.e. everywhere in chinatown) or are place that I only spend a few dollars at.

In the “Double Dipping Via Bill Payment” section of this post, you wrote:

“Free-Quent Flyer reported this last week that this card is now the only Amex card which can be paid at Wal-Mart Money Centers. This opens the Fidelity Amex up to double, triple, or quadruple dipping–charging up this card, and then paying it off to earn even more miles. This is a strategy which doesn’t work for even the big name Amex’s: The Gold PRG, or the Platinum Amex.

Employing a mile earning debit card, and this Fidelity card are surefire ways to earn big miles, at almost no cost besides your time and travel.”

Could you elaborate on how to go about up to quadruple dipping? Also, what mile earning debit cards are recommended (and still available)?

Tim: Sure thing. Aren’t always great Triple/Quad Dip opportunites, but a possible triple dip would be:

Buy With Mile earning CC (1x)

Buy at Grocery store items which earn Grocery Gas rewrds (2x)

Pay Mile earning CC Bill with Debit (3x)

I briefly mention another Quadruple dip possiblity here http://www.milenomics.com/2014/03/using-fuelrewards-and-mastercard-gas/

There’s only 2 mile earning debit cards left–the Suntrust Skymiles card which may/may not still be on offer, and UFBDirect (AA earning).

Thanks for the info on the Saver’s tax credit, although I wouldn’t account for it as a benefit of the Fidelity AMEX per se since any 2% cash back card or other source of income could be used to fund the IRA. It’s certainly important to take advantage of the tax credit if you can, but if you choose to spend the money on something it’s better accounted for as an opportunity cost.

It would be great if you mentioned that Fidelity requires you to spend a significant amount before you get any cash back. $50 is the minimum cash back amount. So if you are getting 2% you need to spend $2500. Spend $2499 and you get nothing. Capital One (and if there are others with a cash back over 1% that do the same please let us know!) offers you a statement credit anytime you request it for any amount you’ve earned so far. Amex and Discover are similar to Fidelity. There are minimum cash back amounts.

Hi Milenomics,

First time to your site through another blog talking about the power of the Fidelity Card. I have a question relating to the BP for the Walmart portion. So basically you use a reward debit card to pay your Fidelity credit card at Walmart? What debit card would you recommend.

Thanks in advance

Hi Bundy, and welcome to Milenomics. To answer your question, yes, the basics are to use a debit card which earns miles to pay the Fido card off. The only two remaining debits which earn miles are the Suntrust Debit card (Delta Miles) and the UFB Direct Debit card (AA miles). The Suntrust card may not be available anymore, so UFB direct would have to be your go to card for earning miles. Unfortunately the limit on UFB direct is $1500 per day, so 750 miles. Also the yearly limit is 120,000 AA miles 🙁

I found your blog just now but better late than never! Interesting write up on the FIA.. am wondering if you compare it with the Priceline 2x Visa ( no annual fee) ? Thank you!

@milenomics

-can you please explain how to actually redeem the points? not as easy as it seems.

-does WM still accept the FIA amex for in-store swipe billpay please?

thanks

Gene: I’m just finishing a post on how to redeem the points. On a Store by store basis some WM do still allow bill payment for Fidelty, others do not. The best way to find out is to call Checkfreepay at 800-676-6148 and ask if your store allows the payment of “Bank of America Consumer loans.”

Anyone else having a hard time getting redemptions at BOA to work with the 75% bonus? I have transferred over Fidelity Amex points over to my BOA travel rewards card, but have not been able to redeem them with the 75% bonus.